Say you’re looking at two investments, one pays 5% each year and the other pays 8%. What is wrong with taking the 8% one? That is what smart consumers do.

And it seems like an obvious decision. You go to buy a TV, one sells for 500 dollars and the other one sells for 800.They both look great so you’ll naturally choose the 500 dollar one.

But what if that 500 dollar TV breaks a week after you buy it?

Similarly, that 5% yielding investment could be a U.S. treasury bond whereas the 8% one a corporate bond and the only reason the corporate bond pays more is because there is a higher risk with the corporation not paying you back your money. And the level of riskiness is decided by the market for each borrowing entity.

But from the borrowing entity’s perspective, it would want to pay the bare minimum it can get away with. Why would it not?

The mistake we make is we look at investments from a buyer’s perspective, just like what we do with other consumer purchases.

We need to instead think like a seller. Ask yourself a simple question. If you were trying to raise money, how much interest would you pay to get someone to give you 100 thousand dollars. You’d want to pay as little as possible.

I’d love to borrow money at zero percent interest rate but the only people willing to lend me that money are my parents. Nobody else is dumb enough to lend me money for nothing.

So when we are chasing yield, the higher we go on the yield spectrum, the greater a chance we won’t see our money back.

Floating rate funds were all the rage right until the 2008 credit crisis hit. Floating rate funds loan money to mostly below investment grade corporations at variable interest rates. They yield more than treasury bonds (they better) but the bond market is not where you go to get rich.

So during the 2008 market crash, when the S&P 500 lost 37%, the average floating rate fund in the U.S. lost 30% while the average high-yield (junk) bond fund lost 26%. By comparison, the Barclays U.S. Aggregate Bond Index of investment-grade bonds gained 5% that year.

And that is what you’d want out of your bond funds. They need to act like a ballast for your portfolio and not sink like the rest of your portfolio.

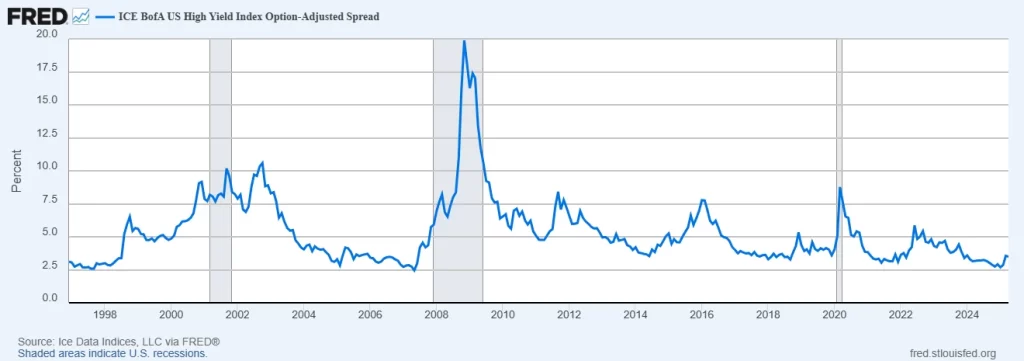

I always look at the high-yield bonds spread to check on the complacency in the market. If investors are willing to lend money to financially shaky corporations for a mere 3% edge1 over treasury bonds, that is not enough compensation for the risk I am taking.

Because if a 2008 type market event happens again, the supposed safe portion of my money that bonds occupy will start to act like stocks which I don’t want.

And the amount of extra yield we get isn’t enough to compensate for the extra risk we are taking. So for the bond side of the portfolios we manage for you, we keep it real simple – no credit risk, no currency risk and limited duration risk. You’ll earn a bit less but with a far higher degree of principal protection. And we’d like to keep it that way.

So if you become our client, we guarantee that you won’t earn the highest returns because that can’t happen with the way we diversify and with the way we emphasize risk as much as we emphasize return. That is a completely different approach than what a lot of people are made to believe from our industry.

Because people are sold high returns with no risk all the time. We know that can’t happen but believing it is when you get killed.

On the other hand, if you only emphasize protecting your money by taking no risk, you will not have the income you need for the many life stages you want to pay for. Only the balance between the two is the right approach.

Thank you for your time.

Cover image credit – Cottonbro, Pexels

- As of March 31, 2025 ↩︎