You are walking down a busy street with your finance professor and you notice a 100 dollar bill lying on the sidewalk. So like any normal person would do, you stoop down to pick it up.

But your finance professor holds you back saying that if that bill was for real, it wouldn’t be there. That is because there are seldom free lunches where money is involved and if you happen to find one, think and rethink as to why you are the only lucky one to find it.

With that as a backdrop, let us now log on to our favorite stock trading app to well, trade stocks. And we know the deal with trading. It is a two-way game. For you to buy, someone has to sell. And that someone is most likely a Goldman Sachs. Or a Citadel. Or a Warren Buffett.

So if whatever you are buying was such a deal, why is the other party selling? Or if whatever you are selling is so bad, why is the other party buying?

Granted, there are always legitimate reasons for that transaction to take place but you keep that in mind every time you trade and you avoid 90% of all the things that can go wrong with your money. For the remaining yet very important 10%, follow along.

The value of a business today is the sum of all the cash flows that business will deliver to you in perpetuity, discounted to today at the right discount rate. The price of a business might get temporarily disconnected from its underlying value but in the long run, it will converge.

This applies to all businesses, public or private. This applies to real estate. This applies to pretty much everything you’d want to deploy your savings into. It is the fundamental law of valuation.

So what explains the volatility inherent with the stock market?

Buying a stock in a business means becoming an owner of that business. That is regardless of how small of a stake you buy in that business. For you to know if you are getting a good deal, you need to get two things right – know the cash flows a business is going to deliver to you and predict the discount rate to use to discount those cash flows to bring them to the present. The math is the easy part but getting these two things right is hard.

Let me explain with the cash flow angle first using two different types of businesses. First, a consumer products business that makes, say mens’ shaving accessories. We are talking razors and blades so a simple business where predicting cash flows should be easy.

Now that business is reliably making those cash flows and suddenly out of nowhere, comes a startup that wants to disrupt that business’s ability to keep making those fat cash flows. Think Harry’s and Dollar Shave Club against the entrenched and comfortable Gillette.

These new startups may offer products that are better or cheaper or both and suddenly the incumbent’s cash flows are toast. Cash flows getting impaired means the value of the business getting impaired and the stock price should follow.

That was an example of the dull and the boring but now, let us explore the same with a newly public, revenue generating but loss-making software business. And you are considering investing in that. They have a great product but will it ever make money? Will it be around long enough to allow you to come up with a fair value for that business? What about competition and what that will do to their profits?

All big questions and hence the price of that business fluctuates more than say a consumer products business. The buyers and the sellers are trying to duke it out in the public markets to arrive at a fair price that is just right – just right based on discounting all the cash flows (dividends) that business will at some point deliver to you in the future and bringing them to the present. We then add up the present values of all those cash flows to arrive at a fair value for that business. Again, the math is the easy part but it gets incredibly difficult to implement.

That explains the challenge with the cash flow aspect of business valuation.

The second and a big one is getting the discount rate right. To explain what a discount rate is, let me start with inflation. We know what inflation is – a rise in prices of goods and services in an economy.

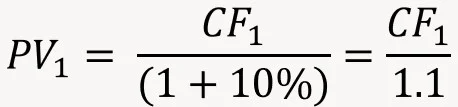

So say the inflation rate is 10%. And you own a business that delivers constant cash flows year in and year out. The inflation-adjusted value of the cash flow today that will be delivered at the end of year 1 then is…

where,

PV1 is the present value of the cash flow a business delivers a year from today and since we are using inflation rate as the discount rate, we can call it inflation-adjusted cash flow in our hands today.

CF1 is the cash flow delivered a year from today.

10% is the discount rate used and in this case, it is the inflation rate.

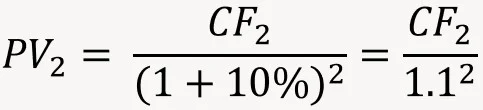

Similarly, the inflation-adjusted value of the cash flow today that the business makes (and delivers to you) two years from now is…

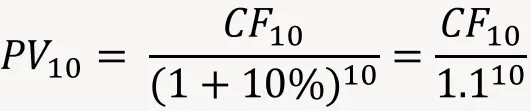

The same math for year 10 cash flow…

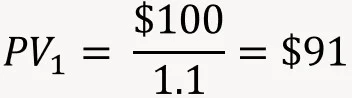

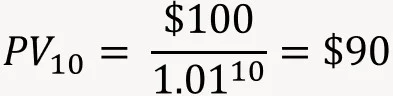

We’ll use some numbers to get a feel for this. Say the cash flow a business delivers is 100 dollars each year forever.

So the value of 100 dollars today that we’ll receive a year from now…

Another way to look at it is when we receive 100 dollars a year from now, it will only buy us 91 dollars worth of stuff. That is what a 10% inflation rate does to our purchasing power.

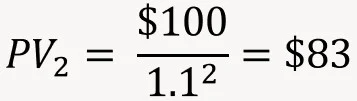

Similarly, the value of 100 dollars today that we’ll receive two years from now…

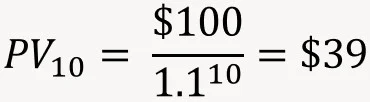

And the value today of the 100 dollars we’ll receive at the end of year 10…

We continue this exercise assuming perpetual cash flows, we add up their present values and we get the value of that business today in inflation-adjusted terms. If the quoted price for that business is lower than the value we derive, we are getting a good deal in terms of being able to outpace inflation. This of course assumes the inflation rate stays the same forever and the cash flows remain constant.

But when inflation is 10%, the interest rates on long treasury bonds should be in the same realm, maybe a bit higher, say 12%.

If super-safe treasury bonds are yielding 12%, why would you invest in anything else unless you get compensated for taking on the extra risk?

So if you are investing in a business with volatile cash flows, you’ll demand a higher rate of return than what treasury bonds yield because why should you not. You need to be compensated for the risk of owning that business so you’ll demand say 15% if it is a large, stable business.

For a small but profitable business, you’ll demand say 20%. For a startup with no proven history of profitability, maybe 30%. Or 50%.

You get the point. The riskier the cash flows, the more you’ll demand in terms of a return. That is discount rate.

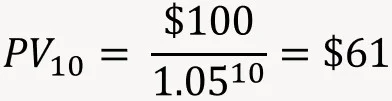

And what if inflation drops to say 5%? Let’s take the year 10 cash flow for the business we were looking at and discount that to today.

So suddenly that same cash flow is worth quite a bit more (it was $39 with 10% inflation rate).

Now instead of 10% inflation, what if inflation drops to 1%. The present value of the 10th year cash flow for that same business then is…

So as inflation rate drops, the value of future cash flows rise.

And as inflation drops, the risk-free Treasury bond rates drop which then means the discount rate used to value a business drops as well and the business’s value hence rises.

So all that thing you see with prices of stocks or for that matter any asset you are thinking to invest in is this tug of war between inflation rate, cash flows and the riskiness of those cash flows.

And millions of market participants are at it every day to get the price of an asset right. Millions if that asset trades publicly for sure. Maybe not as many in the private sphere but the same math applies.

So you have to believe the price of a stock today is pricing in all the information that is out there, past and future. It is a belief and a belief worth believing in.

But what then explains sometimes these crazy run up in prices or steep drops for say some of the publicly traded stocks you own?

- Availability of new information that impacts future cash flows, both on the upside and on the downside. We see that play out with biotech stocks every once in a while when a new drug gets FDA approval. Suddenly, there is a repricing of that business and the stock price hence jumps. Or the stock dives when it fails FDA approval. It might not be evident to you but it is the same discounted cash flow math at work.

- Unexpected events in the economy that causes inflation to change which then results in changes in the discount rate which then impacts asset (stocks, bonds, real estate) prices.

- Animal spirits and momentum driven changes that impact short-term movements of prices. This we don’t care much for because it is not durable or predictable. And the prices eventually revert to what the business is truly worth in the long run.

So markets can act irrationally in the short run and they do from time to time, but you don’t care and you should not care if your time horizon is long.

And if you believe that markets are efficient even though they are not perfectly efficient at all times but you should act as if they are, then the only logical conclusion is that all risk assets should have similar risk-adjusted returns. Not similar returns but similar risk-adjusted returns. Bonds are riskier than cash and hence should yield more. Stocks should yield more than bonds because they are riskier and so on.

And the circus you see play out in the markets every once in a while, just be amused and watch from the sidelines. Because as Jack Bogle once said, the stock market is a giant distraction from the business of investing.

Don’t let the markets distract you away from what good investing is truly about.

Thank you for your time.

Cover image credit – Bo Minh, Pexels