Individual health insurance was the hardest thing to buy in the past. You didn’t have a human resources department or a fancy benefits consultant watching out for you so it was really easy to accidently end up with a really bad insurance.

And though complexity still remains, the buying part is reasonably sorted out with HealthCare.gov. You go on there and look for individual plans for your state. The experts working there have screened out all the bad ones so you are reasonably safe.

Health insurance is regulated, priced and sold on a state by state basis. Where you live matters in terms of how much insurance is going to cost you and what kind of benefits you can avail.

All health insurance policies pay full upfront costs for preventive care. Insurance companies are also required to spend 80% of the premiums they collect on your medical care instead of on red tape so you’ll get more value for your dollars.

And they are required to insure you regardless of any pre-existing conditions. Plus there are no caps on how much they are going to pay for healthcare in a given year or during your lifetime. That is if you get real health insurance and not junk insurance.

On that note, there are no bargains with health insurance. If you are shopping on your own and you find a policy that is a good amount cheaper than the rest, there are only two possibilities. Either it carries a super high deductible or you are about to buy some junk insurance.

Junk insurance looks like health insurance but it isn’t. Typically, it is a policy that only pays out a set amount for an individual service. For example, a lot of policies will pay out $300 a day when you are in the hospital but hospital stays can cost $5k or $10k a day so if you have one of these policies, you can be in the poorhouse in no time.

There are three broad categories of health insurance: HMOs, EPOs and PPOs.

HMOs are ideal but they get a bad rap because of restrictions when going out of network. That is all true but if you find an HMO with a good network, it is worth considering because HMOs are usually more affordable, especially for families who have to run to the doctor all the time. They don’t have big deductibles.

PPOs give you more choice of doctors. You can go out of network if you want assuming you can afford the high deductibles that accompany that choice.

EPOs are somewhere in between.

When deciding on the right insurance for your family, you need to consider the total package. What is the deductible on your plan? What co-pays will you pay for things like doctor visits and prescription drugs.? What percent of the hospital bill you’ll have to pay? You need to add up all of this to assess the true cost of insurance if you were to get seriously ill.

Another thing you want to know is the out-of-pocket limit. It is the most you’ll pay for healthcare in a given year. I know all this sounds confusing so we’ll walk through a case study to show how this all works.

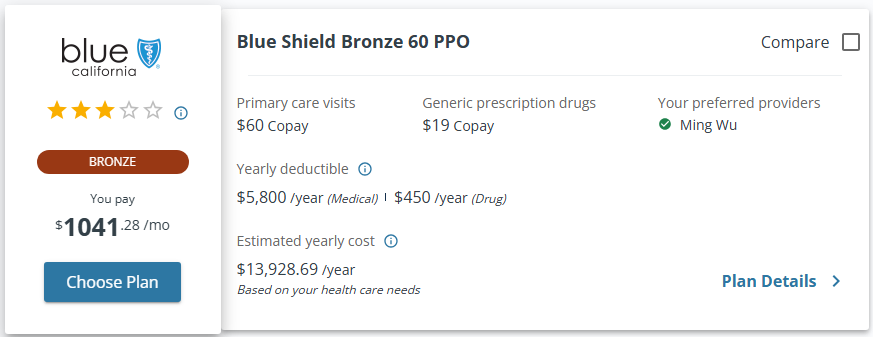

I pulled this quote from the Covered California link that you get automatically redirected to when you enter your zip code at the HealthCare.gov site. This is for a family of four making $150,000 a year.

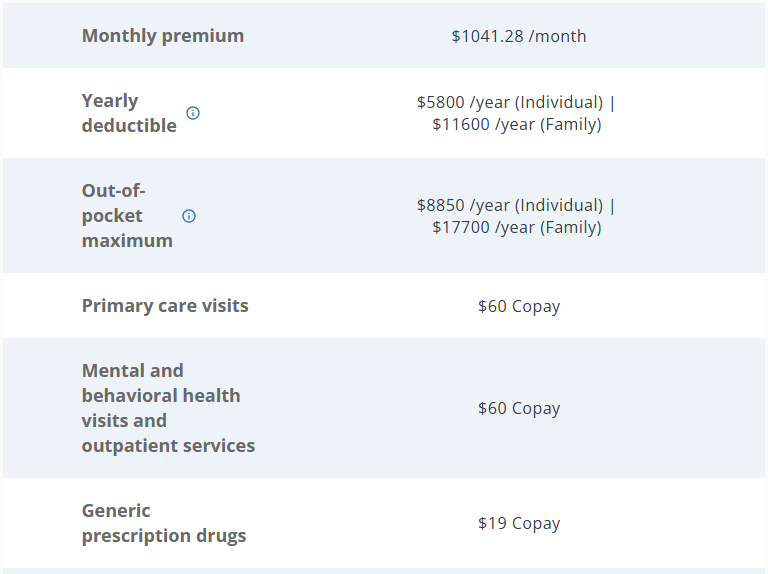

Click on Plan Details and it leads you to a page that describes everything you’d want to know about that policy. The snapshot below is just a small but important segment.

The monthly premium is clear. That is what you pay each month for insurance. Family plans have both individual and family deductibles. The outline below describes how to interpret some of these numbers.

- Each family member has an individual deductible. Then there is a family deductible on top. All individual deductibles funnel into the family deductible.

- The family deductible can be reached without any members on a family plan meeting their individual deductible.

- For example, for a family of four, ½ individual deductible + ½ individual deductible + ½ individual deductible + ½ individual deductible = family deductible.

- If two family members reach their individual maximum out-of-pocket, all members are covered 100% at no additional cost through the end of the plan year.

- For example, individual maximum out-of-pocket + individual maximum out-of-pocket = family maximum out-of-pocket.

Let us see how this works for the plan described above for that same family of four we pulled the quote for. Husband is age 36, wife is age 34, daughter #1 age 6 and daughter #2 age 3. The family is expecting a 3rd child any minute. I have summarized all the costs this family may incur when using the coverage. This is besides the monthly premium payments that must be paid.

- Co-pay: $60

- Coinsurance: 40%

- Individual deductible: $5,800

- Family deductible: $11,600

- Individual maximum out-of-pocket: $8,850

- Family maximum out-of-pocket: $17,700

We’ll walk through a set of scenarios this family experiences during the course of a year and see how the expenses flow into the deductibles and family max out-of-pockets.

- Husband breaks his leg playing soccer and goes to the emergency room for treatment. It costs $2,800 which goes towards his individual deductible and the family deductible. It will also apply toward the individual and family max out-of-pockets. He is responsible for 100% of these charges because he didn’t meet the individual deductible yet.

- Wife delivers a baby. Including postpartum care, the total bill comes out to $19,800. She pays $5,800 to meet her deductible, which also goes toward the family deductible as well as individual and family max out-of-pockets. The remaining balance applies to coinsurance and she is responsible for 40% totaling $5,600 for a total out-of-pocket cost of $11,400.

- $5,800 deductible + $5,600 coinsurance = $11,400 total wife would pay.

- The family deductible amount that is met increases to $8,600 (Husband $2,800 + Wife $5,800 = $8,600).

- Daughter #1 was taken to urgent care with a 102-degree fever. The urgent care visit carries a co-pay of $60 and she gets a generic prescription costing $15. Office co-pays and pharmacy do not count towards deductibles but do count towards the out-of-pocket maximums.

- The family deductible amount that is met remains at $8,600 (Husband $2,800 + Wife $5,800 = $8,600).

- Daughter #2 is rushed to the emergency room due to acute abdominal pains. After a series of tests, it was discovered that she’ll need surgery to reverse an intestinal abnormality. Her bill comes to $3,600.

- After paying $3,000, the family deductible is met (Husband $2,800 + Wife $5,800 + Daughter #2 $3,000 = $11,600).

- Daughter #2’s remaining balance of $600 is covered at 60% after paying the 40% coinsurance of $240.

The entire family will now only pay coinsurance and co-pays until they meet the maximum out-of-pocket or when the plan year ends. Based on all the costs this family has incurred, they’ve met $11,675 of the family maximum out of pocket limit of $17,700.

- Husband $2,800 + Wife $5,800 + Daughter #1 $60 (co-pay) + Daughter #1 $15 (prescription drugs) + Daughter #2 $3,000 = $11,675.

So when you’re trying to determine the overall cost for the year, keep this in mind. The least you’ll pay is your 12 monthly premium payments. The most you’ll pay is your 12 monthly premium payments plus your out-of-pocket maximum. That is the range you should use to budget for healthcare in any given year.

All this may sound confusing but it is a lot better than it used to be.

Thank you for your time.

Cover image credit – Pixabay