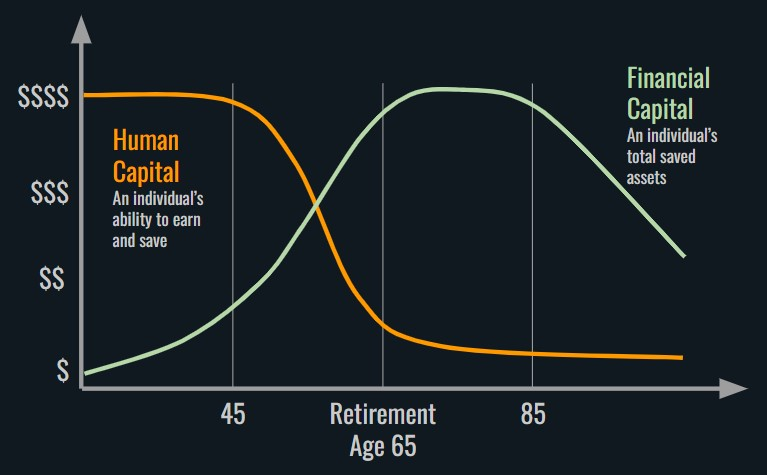

When you are young, your ability to earn income represents the largest portion of your total wealth. Your ability to earn is your human capital. Your financial capital, on the other other hand, barely amounts to anything as you haven’t had much time to accumulate it yet.

But as you age and progress through your career, you slowly convert your irrecoverable human capital into financial capital that’ll help fund your lifestyle in retirement.

Your human capital is more a bond-like investment considering all the future paychecks it is going to generate. In fact, your human capital is more like an inflation-indexed bond as your paycheck is expected to rise with inflation. And if you were to nurture your human capital well, it can be even better than an inflation-indexed bond as you can make your paycheck rise more than the rate of inflation.

So from a portfolio allocation perspective, your total wealth is more bond-heavy when you are young. You can’t screw up much as you don’t have much financial capital to screw up.

But as you age and as you convert your human capital into financial capital, mistakes can be fatal. You can find many stories of folks having to start over at the tail end of their human capital curve due to poor investment decisions.

And poor investment decisions mostly come down to not understanding what you own in your portfolio, why you own it and what purpose does a given investment serve in the grand scheme of generating the income you’ll need in the most tax-efficient way possible.

And instead of owning portfolios that are just right for one’s station in life, we make bad market timing calls like going to cash when we feel the market is too richly priced as if we can know what the true price is. We don’t.

I’ve found variations of the bucketing approach to be a reasonable guide in building up to a financial base that will help deliver on your retirement income goals.

- Bucket 1: Six months to two years worth of living expenses in near-cash instruments like Treasury bills and CDs. Count income from sources like Social Security and pensions in the mix and the difference is what you’ll need to fulfill your Bucket 1 requirement. If you have been religiously buying I-bonds over the years, that could be your Bucket 1 money until it’s exhausted.

- Bucket 2: Another 8-10 years worth of living expenses over and above other income sources invested in a good mix of high-quality bonds.

- Bucket 3: The remainder of the portfolio invested in a diversified mix of global stocks. Some include the nicely worded high-yield bonds in the mix but their true definition is junk bonds and taking risks with the bond side of the equation is rarely worth it.

Income and rebalancing proceeds from Buckets 2 and 3 are used to replenish Bucket 1 as it gets depleted.

You may not need to follow this precise recipe if income from other sources plus income from stock dividends liberally cover your expenses. In that case, your approach to portfolio building takes a legacy-building mode as you won’t be able to use all your money.

But whatever the case maybe, the decisions you make at the tail-end of your human capital curve are irreversible in nature. There are no do overs so a great deal of thoughtful planning is a given, not just when you retire but in leading up to that point and through retirement.

Thank you for your time.

Cover image credit – Feyza Dastan, Pexels