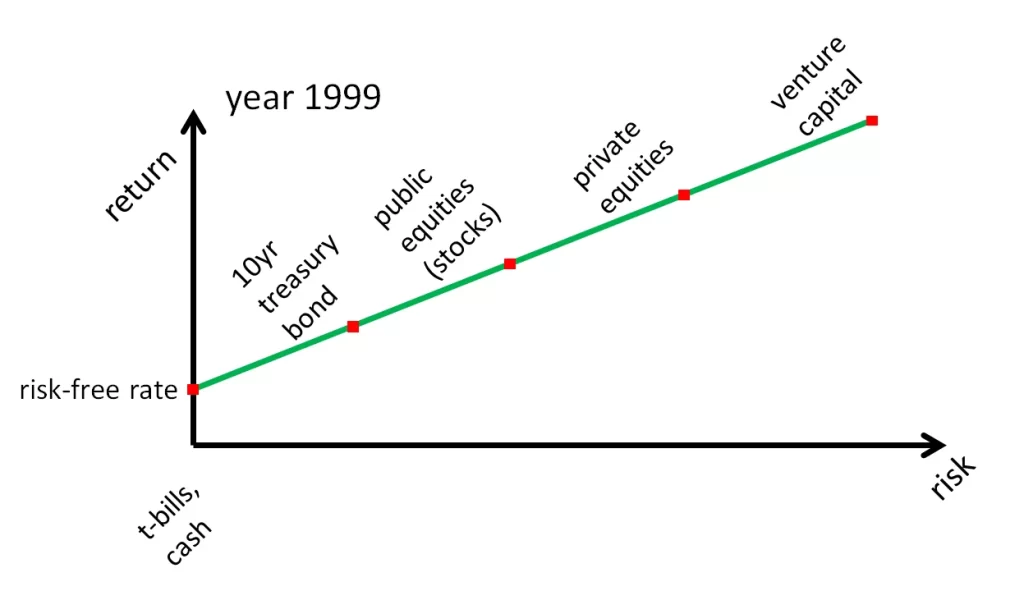

Treasury bonds are issued by the Federal government. Bonds with a maturity of one year or less are called Treasury bills but they are still bonds.

So, say the year is 1999 when a one-year Treasury bond pays 4% interest. If a bond with a maturity of one year pays 4%, you would expect more payment from a five-year Treasury bond. Five years is a long time to wait to get your money back.

The five-year bond hence must pay like 6% interest else why would you take the risk of locking up your money for that long.

And if the five-year Treasury bond pays 6%, the same maturity corporate bond must pay higher. Corporations can go out of business, governments don’t.

Following along that risk-return spectrum, you would demand an even higher interest rate from an issuer of the same maturity junk bond, also called a high-yield bond. This is the investment world’s equivalent of putting lipstick on a pig but do not be fooled by the pleasant sounding high-yield term. Junk bonds are issued by businesses that are on the verge of going out of business.

The riskier the issuer of a bond hence and/or the longer the time to maturity of that bond, the higher the rate of return you should expect.

And if a blended portfolio of bonds yield whatever it yields, publicly traded stocks must yield more. Stocks are riskier than bonds because cash flows (dividends) from stocks are not guaranteed whereas interest income from bonds usually is. And in the event of a bankruptcy, bondholders come before stockholders on any claims on business assets. So, stocks in theory should earn more than bonds.

If public stocks yield whatever they yield, venture investments must yield more. Venture investing means investing in nascent, not yet proven businesses where profits don’t exist yet. There is also illiquidity risk where unlike publicly-traded stocks, you can’t just wake up one day and decide to sell your investments. That is a roundabout way of saying that you should expect a higher rate of return from venture investments than other types of investments because they are the riskiest.

The risk-return relationship just described is the Capital Markets Line and it looks something like this…

Treasury bills (risk-free rate) are the shortest maturity and the safest of all investments. Venture capital is the longest maturity and the riskiest of all investments.

And you’ve probably heard that the more risk you take, the more return you’ll earn.

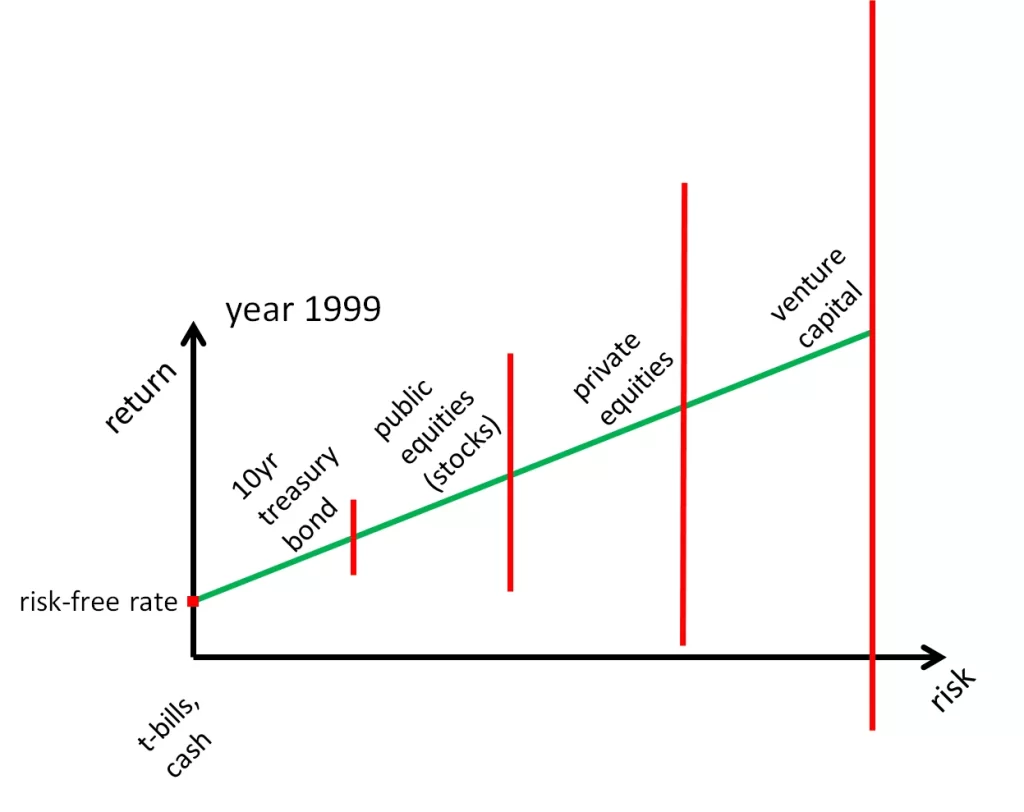

But if riskier investments could be counted upon to deliver more returns, by definition, they wouldn’t be riskier. The prices of those investments would be bid up to a point where no net return above the risk-free rate exists. So, the more risk equals more return theory does not quite hold.

The correct way to formulate the Capital Markets Line then is…

There is now a distribution of returns instead of point estimates for each investment. The riskier an investment, the wider the distribution of potential outcome of returns.

Howard Marks in his book, The Most Important Thing talks about this and this quote from that book captures the essence of the reconstituted Capital Markets Line…

The correct formulation is that in order to attract capital, riskier investments have to offer the prospect of higher returns, or higher promised returns, or higher expected returns. But there’s absolutely nothing to say those higher prospective returns have to materialize.

Howard Marks

Prospect, promised, expected mean the same. Investments that are riskier must appear to offer higher returns. They don’t necessarily have to deliver on that promise though.

So that was the world of 1999.

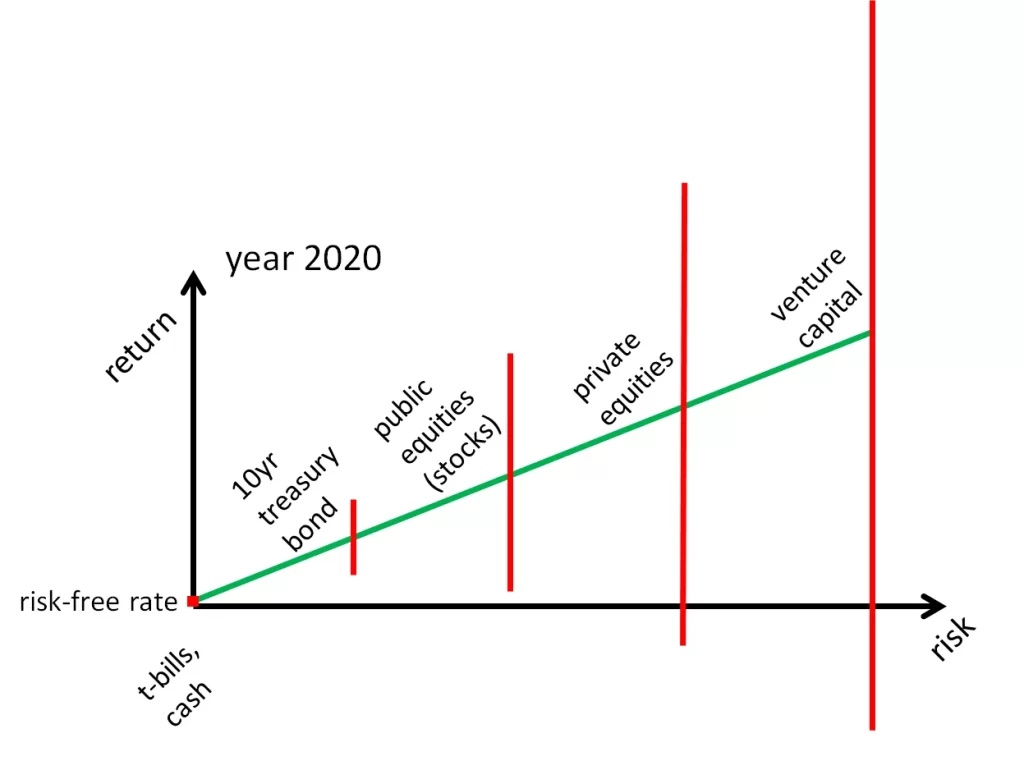

Then we had some interim booms and busts so the Federal Reserve, in their attempt to make sure the economy doesn’t collapse, floored the interest rates to zero.

The updated Capital Markets Line following that…

So the entire line shifted down, which means the discount rates (expected rates of return) for each one of those investments moved down as well.

And since discount rates are in the denominator of any valuation analysis you’ll do and when they go down, investment values go up. The 4% bond you now own is more valuable when the market interest rate for a new bond is zero.

But when market interest rates rise again which they did these past few years, we start to go back to the 1999 interest rate regime which then means discount rates rise and consequently, investment values fall. Projects and investments that penciled out when interest rates were zero may no longer do when interest rates are higher.

But then your future expected return on any new money you invest is higher. The time to invest is when investment values are lower and expected returns are higher. That is counter to how we behave but that is human nature doing what it always does.

Thank you for your time.

Cover image credit – Cottonbro, Pexels