Benjamin Graham lived a remarkably productive life. Besides being one of our nation’s Founding Fathers, he was a prolific author. He was also a scientist, an inventor, a printer, a postmaster, a humorist, a statesman and a diplomat. His daily schedule as recorded in his autobiography is one for the keeps.

His relationship with money was equally inspiring. He viewed money not just as a means to personal wealth but also as a tool for societal good and progress. He believed that hard work, saving and wise investing were essential for both individual prosperity and the betterment of society.

He is credited with timeless money quotes like a penny saved is a penny earned and money makes money, and the money that makes money, makes money.

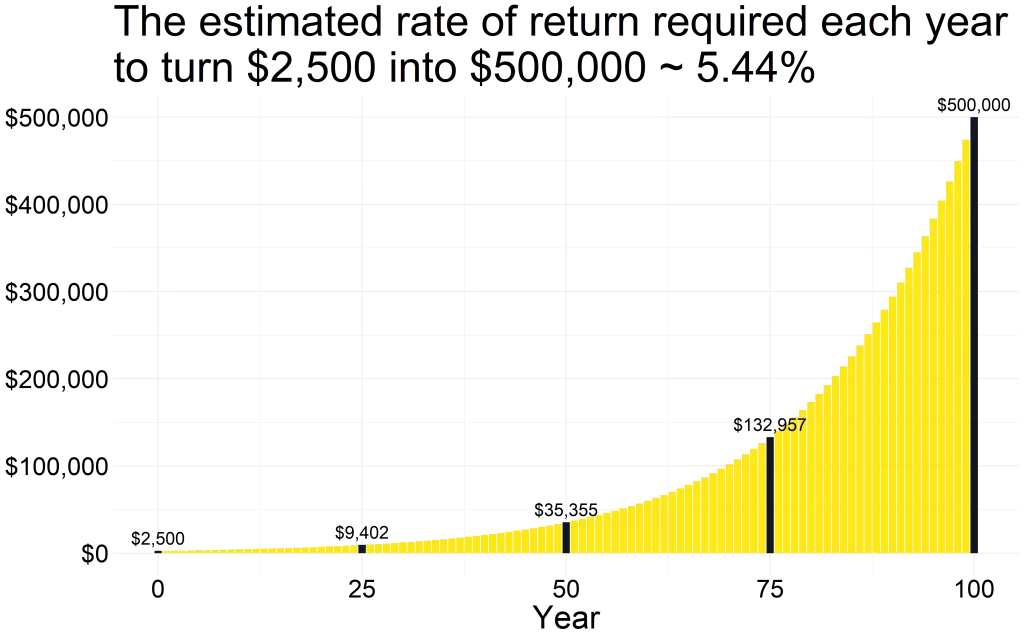

He died in 1790 and left his life savings of $10,000 to be equally split between two of his favorite cities, Boston and Philadelphia. But he left the money with some strings attached. The first half of the money that each city received should be invested and can only be used after 100 years. And the second half after 200 years.

In 1890, at the end of the first 100-year period, each city received $500,000 to be spent on public goods. That is what $2,500 turned into after 100 years of compounding growth.

And since the money was invested like how a bank invests, the rate of return it took to turn $2,500 into $500,000 in 100 years was a respectable but not outlandish 5.44% each year. Time did the rest of the work.

Exponential growth which compound interest is an example of, is hard for us to intuitively process but exponential growth is where magic happens. Take for example the first 25 years in the plot above. Nothing much happens there. The last 25 years feel magical.

In 1990, after 200 years that Mr. Franklin required the money to remain invested, each city received the remaining bequest. Any guesses how much the other $2,500 turned into? 20 million dollars.

And again, you’d think you’d need some impressive investing skills to do that. Nope. It took a relatively modest 4.6% rate of return each year but doing that for 200 years is what did the trick.

Granted, we don’t live on 200-year timelines but if you have been investing for a couple decades, you are likely seeing the fruits of compound interest take hold with your own money. Like you’ll see years where your money makes more money than what you make in your paychecks.

Greek mathematician Archimedes once theorized that if he had a lever long enough and a fulcrum on which to place it on, he can move the world. Time is the Archimedes lever of investing.

Warren Buffett is in his nineties and is a really rich man. But 99% of his wealth came after his 50th birthday. And no one knows compound interest better than him.

When my daughters were little, I would present the compound interest math at every chance I got. And playing around with it is quite fun.

FV = PV x (1 + r)t

FV is the Future Value of your savings

PV is the Present Value

r is the rate of return

t is time

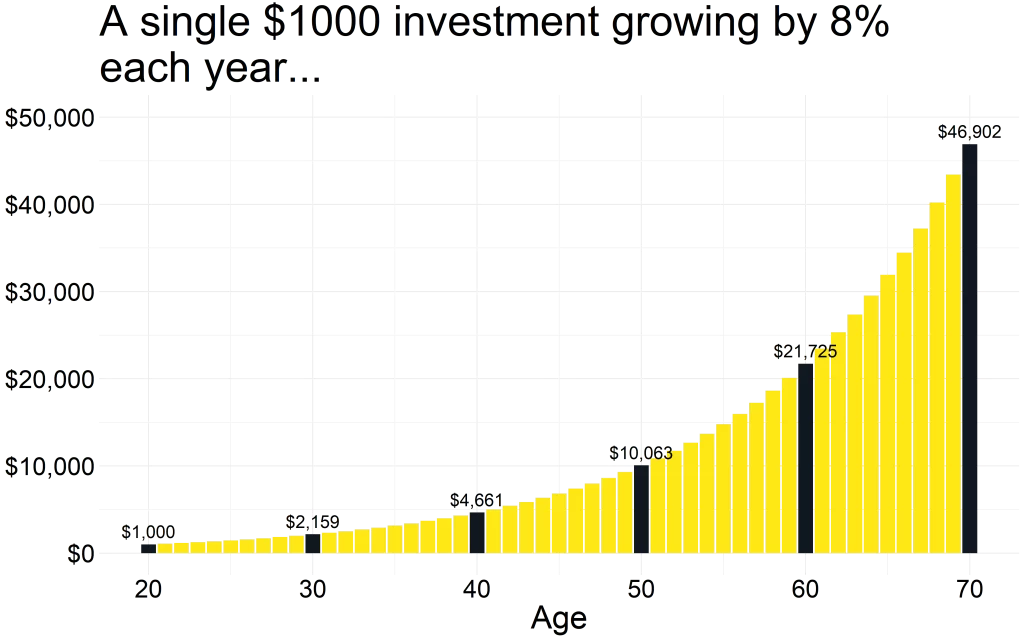

Say I start with $1,000 (PV) at age 20 and earn an 8% rate of return (r) on it each year. In 5 years (t), that $1,000 will grow to $1,470 (FV). No big deal.

But in 30 years when I am age 50, I’d 10x my original $1,000 investment. In another 10 years when I turn 60, I do 22x my original investment.

And think about this. I make more money in the last 10 years after I turn 60 than the previous 40 years combined.

Amazing, isn’t it? Compounding growth during the early years is painfully slow and that is when many give up. But stay on that path long enough and you won’t believe your bank accounts.

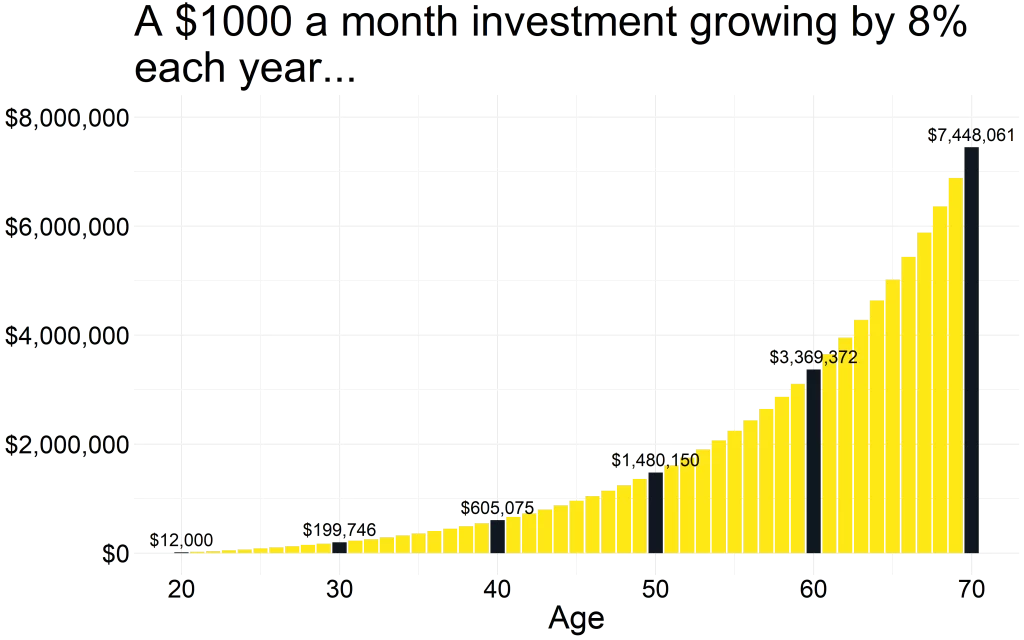

Now imagine instead of a single, one-time investment, I invest $1,000 each month starting at age 20 and do it for the next 50 years.

This is fully-funding a great retirement even when accounting for inflation. All it takes is some small early sacrifices and time takes it over from there.

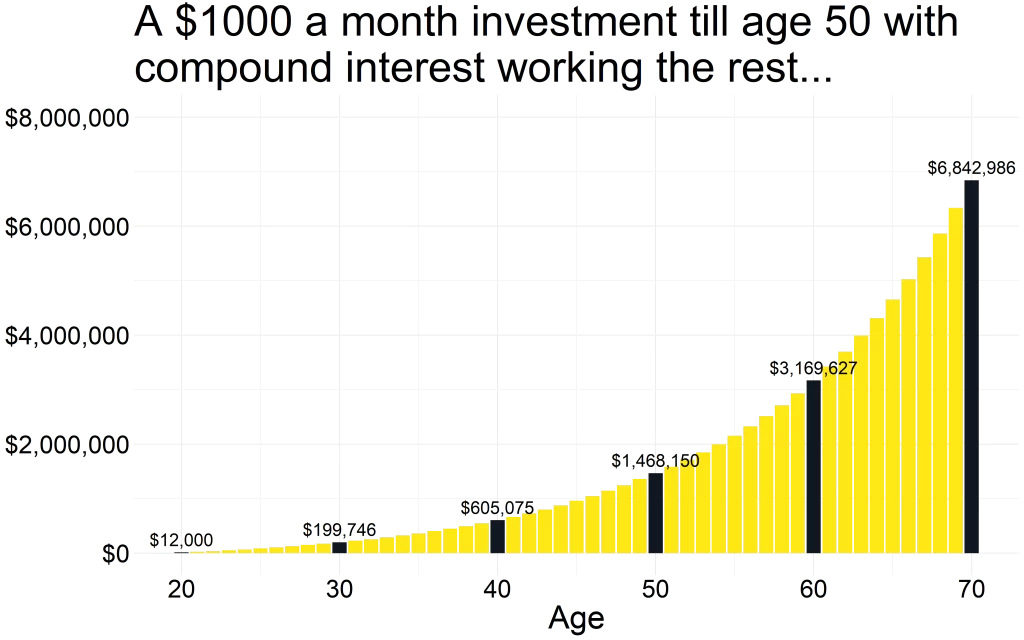

Because when money makes money on money, you reach a stage in life where your accumulated savings do the hard work while you coast. Like say I start with investing the same $1,000 a month at age 20 but stopped at age 50 instead of continuing to save till age 70, how much of the last 20 years of not saving anything matter?

Apparently, not much.

Early contributions matter way more than contributions that come later.

A thousand dollars a month appears big money to save, especially when in your 20s but if you’ve got a half-decent 401(k) plan at work with an employer match to boot, I guarantee you won’t even feel it. You just need to start. The Archimedes lever does the remaining work.

Thank you for your time.

Cover image credit – Pixabay