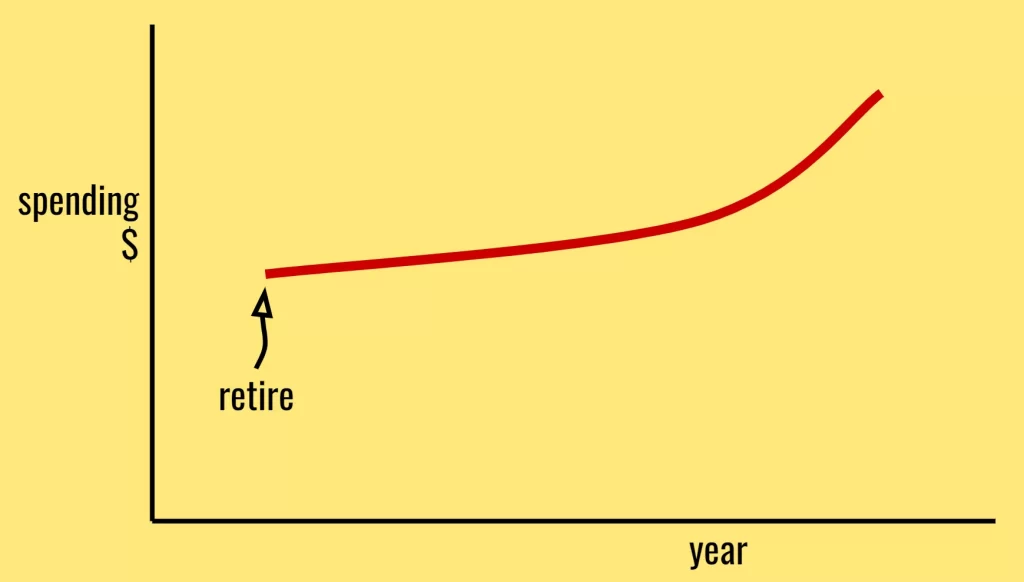

You think you’ll spend like this…

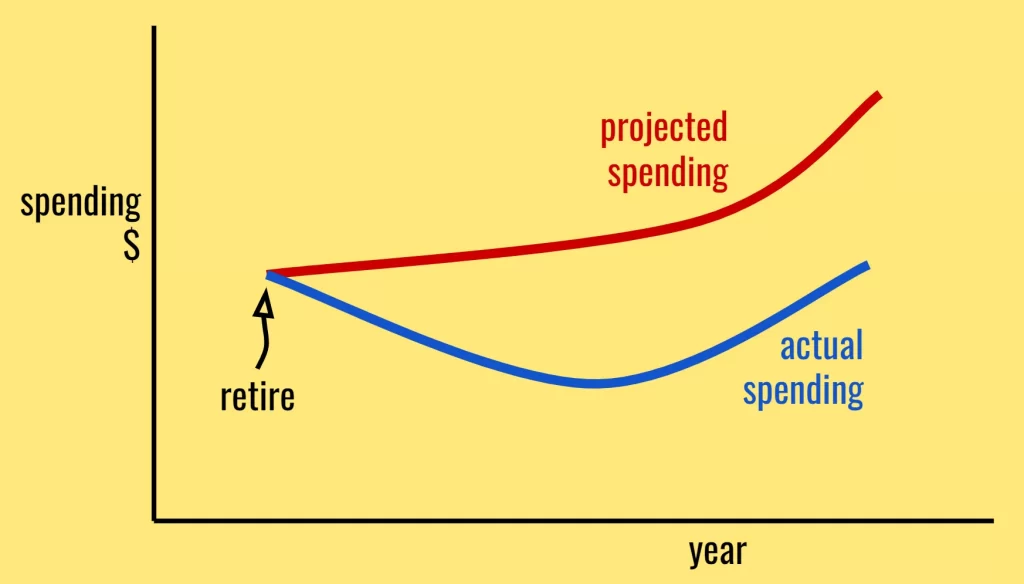

But instead, you spend like this…

This is not just anecdotal. J.P. Morgan found that most retirees spend less as they age, not more.

And it makes total sense. Retirement experts who’ve studied this say that we spend in three phases…

- the go-go years,

- the slow-go years,

- and the no-go-years.

The go-go years are your first set of years in retirement. You play, you travel, you spend.

Then you start to slow down. Your spending naturally declines.

And then you really slow down. But your spending rises as you start to spend more on healthcare. That rise though gets cancelled by reduced spending in other areas of your life.

The plans I design for you assume a constant 3% growth in spending each year to account for inflation in retirement. J.P. Morgan found that the actual rise in spending tracks more like 1.8% each year.

That is a big change. Let me explain why.

Say you are 45 today and expect to retire at 65 and say you need $100,000 a year (in today’s dollars) at retirement. Assuming 3% inflation, if you need $100,000 today, you’ll need $180,000 when you retire in 20 years.

But if realized inflation is only 1.8%, the same $100,000 will only cost $143,000 at retirement. Assuming 4% safe withdrawal rate, you’ll now need to save up to a $3.5 million investment portfolio instead of $4.5 million before.

That is a million dollars in extra savings you don’t have to do. I have talked about health life expectancy before and it peaks at around age 62. Imagine what you could do with an extra million at the peak of your prime.

Your plans are intentionally conservative and if you follow them to the tee, you’ll leave a bunch of money behind. Because what you don’t spend will compound for decades into an enormous sum later.

Not the worst of problems to have but you may not want those problems if it comes at the expense of your definition of a good life today.

Thank you for your time.

Cover image credit – Kat Smith, Pexels