Say someone you know is running short on funds and comes to you for a loan that he promises to pay back in a month. Will you lend him the money? And if so, will you do it for free?

You’d say why not. You have loaned him money before and without fail, he pays you back on time.

But say that same someone comes to you for a loan that he promises to pay back in a year? Would you loan him the money for free then?

It is different this time. Money loses value over time due to inflation so waiting a year means you are losing purchasing power.

And now say that someone comes to you for a loan that he will pay back in 10 years. This is now way different, not only in terms of the purchasing power lost but also the likelihood that you may not see your money back.

And because of that, you’ll demand a much higher interest rate on your loan.

Something similar plays out in the bond market. When you lend money, you are in fact buying a bond regardless of whether you are lending it to a friend, to a government or to a business. They do have different risk profiles as they should but inherently, it is the same thing.

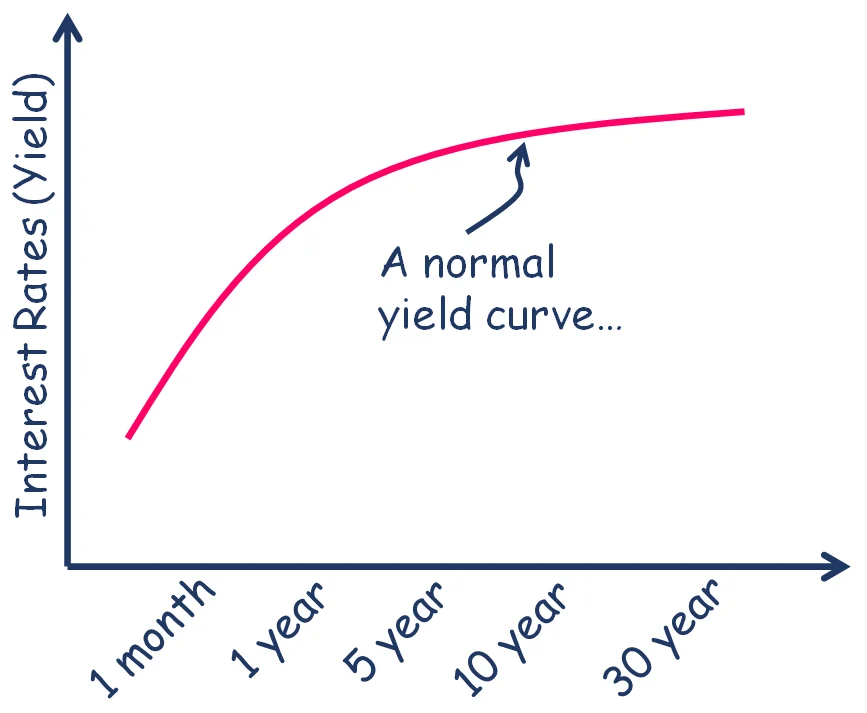

United States treasury bonds are the safest of all bonds you can buy. They range in maturity from 30 days to 30 years. A bond matures when the loan term ends.

So, between say a 30-day bond and a 30-year bond, which one do you think should pay a higher interest rate? The 30-year bond, of course.

A lot can happen in 30 years whereas not much happens in 30 days. By investing in a 30-year bond, you are giving up access to your savings for a much longer timeframe, hence a much greater risk.

And in return, you’d demand a higher interest rate. Interest rates gradually sloping up as bond durations rise makes intuitive sense. That is the yield curve or that is how a normal yield curve should behave.

Now when short duration bond yields rise while long duration bond yields stay the same and they rise to a point where now both the short and the long duration yields are the same, that is a flattish yield curve. It does not make logical sense that that should ever happen but it does.

But when short duration bond yields rise to a point where they are now higher than the long duration ones, that is an inverted yield curve. That never makes sense but it happens.

But why would a yield curve flatten or invert? Before that…

A primer on how your local bank or credit union makes money…

To you as a customer, there is no difference between a bank and a credit union. A bank is a for-profit enterprise, owned by shareholders whereas a credit union is customer-owned and run as a non-profit. So if you bank at a credit union, you are also a micro-owner of that place. The money that a credit union earns is passed down to you in the form of lower fees and lower costs for loans you might take out.

So with that out of the way, when I refer to a bank, I am referring to both types of institutions.

And a bank’s business model is simple. It takes in deposits that are usually short-term in nature and makes longer-term loans against them.

Short-term interest rates in normal economic times are lower than long-term rates and that difference is a bank’s profit.

When a bank makes bad loans…

A bank’s business model is predicated on the fact that it does not make too many bad loans. Because if it does and sometimes even if it doesn’t but depositors suspect that it did, the depositors will all rush in at once to take their money out.

But if everyone rushes in to get their money out (a bank run), the bank goes belly up because it does not have the cash to pay out. It has all been loaned out.

And that is why the Federal Reserve requires each bank to have a minimum amount as reserves on hand. That reserve requirement is typically set at 10% of the total deposits a bank has on any given day but that requirement varies based on what the Fed decides.

This means that a bank with $1 million in customer deposits must maintain at least $100,000 as reserves. It can then lend the remaining $900,000 to borrowers or to other banks. Throughout the course of a day, new deposits are made at the bank and new loans are given out but when the day ends, the bank must tally up its books to make sure reserve requirements are met.

The federal funds rate, also called the overnight rate…

But if more withdrawals were made than deposits, the bank may find itself short on reserves like say by $50,000. It would then have to borrow the $50,000 overnight as a short-term loan to meet the regulatory requirement of the 10% reserve threshold.

And if another comparable bank saw more deposits than outflows, it may find itself with say $150,000 available and so it could lend the excess $50,000 to the bank that is short on reserves.

And why would it not? Why not earn a small amount of income on the excess deposits rather than have it sit in bank vaults as cash earning nothing.

The rate at which banks lend to each other on an overnight basis is called the federal funds rate and that rate is set by the supply and demand in the market for these kinds of loans. If the supply of reserves is greater than the demand, the federal funds rate falls. And if the supply of reserves is lesser than the demand, the rate then rises.

The discount rate…

If there are no banks with excess reserves or if the banks are unwilling to lend to the bank in need, that bank can then instead borrow directly from the Federal Reserve at a rate called the discount rate. And just to make sure we don’t confuse ourselves more than we already are, this discount rate is different from the discount rate we use to do discounted cash flow analysis.

This discount rate becomes the target interest rate for the federal funds rate. It is usually set higher than the target federal funds rate because the Fed prefers that banks borrow from each other than from itself. The Fed would rather have the banks continually monitor each other for credit risk instead of them intervening.

And since the discount rate is set higher than the federal funds rate, quite naturally the banks wouldn’t want to borrow directly from the Fed. That borrowing is only intended as a backup source of liquidity for healthy banks who might need the money on an overnight basis to meet their reserve obligations.

The Fed also makes sure that the federal funds rate never rises too far above its intended target by using the discount rate as a ceiling for the federal funds rate. The discount rate hence, is the primary tool by which the Fed controls money supply in the economy.

The Federal Reserve’s charter…

The Federal Reserve’s main job is to make sure that the economy has full employment and stable prices. That is, the Fed wants anyone looking for a job to be able to find one while ensuring that inflation remains tame and deflation never takes hold.

And they engineer that by changing the level of reserve requirements and/or by manipulating the discount rate they pay banks for excess reserves.

So when the economy is running hot which can cause hyperinflation, the Fed raises the discount rate which then increases the federal funds rate banks charge each other for excess reserves.

So if I am running a bank and have excess reserves, I might as well park the money with other banks or with the Fed then take the risk of lending it out. Lending to consumers and businesses hence slows which then causes the economy to slow and that helps keep inflation in check.

On the other hand, when the economy is stagnant or growing slowly, the Fed may reduce the discount rate in an effort to make borrowing more affordable for member banks. That then reduces the incentive for banks to keep more reserves with other banks or with the Fed and instead loan them out. Consumers and businesses get access to cheaper loans which they put to work, resulting in an increase in economic activity.

So when we hear about the Federal Reserve raising or lowering interest rates, we think they control all interest rates. But they only control the discount rate. Longer term rates like what we pay for mortgages and car loans are at the mercy of the markets, their expectations of growth rates and long-run inflation.

The QE effect…

Recall again a bank’s business model. It takes in short-term deposits and makes longer-term loans. The spread between short and long-term interest rates is how a bank makes money. The bigger the spread, the more profitable loans become.

So when the yield curve is steeper (lower short-term rates and higher long-term rates), lending is more profitable. Banks then have an incentive to lend more and more money. The quantity of money in an economy hence grows which is then followed by increased economic activity and growth.

When the yield curve flattens, lending is less profitable and banks lend only to the safest of all customers. Because when the payout is low, risk taking takes a backseat. That slows the velocity of money (how fast money changes hands) in an economy which then slows economic activity.

When the yield curve inverts (short rates exceed long rates), lending isn’t profitable so banks curtail lending and the economy grinds to a halt.

Banks are the main gatekeeper of capital in an economy and they do a fairly good job of assessing loan risk. That is not always the case as what we saw during the credit crisis of 2008 when the entire banking system was in trouble because too many bad loans were made.

To stave off that crisis, the Federal Reserve along with lowering the discount rate (short-term rates) also engineered to lower longer-term rates by intervening in the bond markets. They went in and aggressively bought long-term treasury and mortgage bonds. That is quantitative easing or QE as it came to be called.

And when demand for bonds rose, their prices rose. Bond prices and interest rates are inversely related so consequently, long-term interest rates fell. Lower long-term rates made lenders of all stripes less eager to lend which showed up in data during the decade of 2010s when economic growth was the weakest in modern history.

This corrects itself with time as the Fed learns from the many experiments it tries to maintain a healthy economy. And they know that they cannot and don’t want to take ownership from banks as the gatekeepers of capital.

But not much about what happens with the shape of the yield curve matters to our long-range financial plans unless it presents opportunities that we can capitalize on. Else we watch from the sidelines and sit tight.

Thank you for your time.

Cover image credit – DreamLens Production, Pexels