Peer-to-peer lenders make lending to individuals and businesses easier without needing a bank in the middle. But banks play an important role in assessing credit risk so if banks don’t want to play this game, you shouldn’t either. That is more true if you plan to lend big money.

Because if it is not a good enough deal for banks who are in the business of lending money, why would it be a good deal for you? Granted, banks are not going to want to lend a couple hundred dollars but if you are lending serious money, I’d reconsider.

Because in finance as in life, there is often a huge chasm between what is expected and what actually happens.

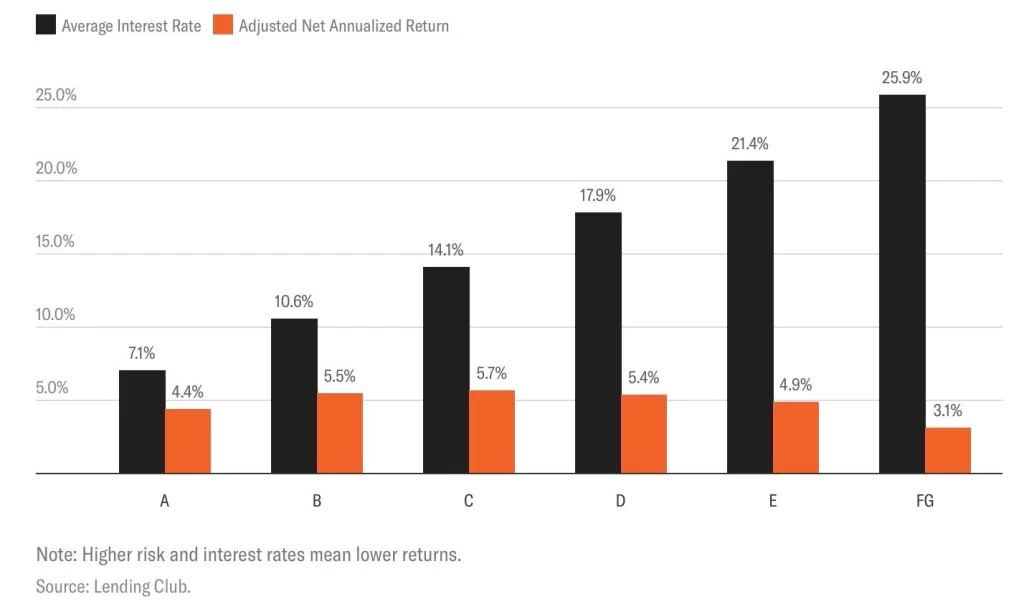

This is aggregate data across the entire platform and as is evident, not everyone who borrows pays back their loans. So even when the promised rate of return is 25.9 percent, the actual realized rate of return is far lower and oftentimes worse than what you can make on safe treasury bonds.

That is because a big chunk of the folks who borrow at high interest rates, don’t pay back their loans. Why must they borrow at such high rates? Because they have sketchy credit records and LendingClub hence categorizes them as high risk borrowers which comes to be true.

Something similar transpires in the credit card industry. Credit card companies make unsecured loans to borrowers and because the loans are unsecured, they charge elevated interest rates. But the effective rate of return the credit card companies earn on their loan portfolio is likely similar to what the LendingClub data shows.

But if the same set of customers were to borrow money for homes and cars, they will be charged much lower rates because these loans are secured by an underlying asset (a home or a car). Miss a few payments on your home or car loan and the bank seizes those assets.

Stocks that pay unusually high dividends suffer from similar problems. If a diversified portfolio of stocks pays a 2 percent dividend yield and you come across a stock that pays 5 percent, there could be a problem. The business behind that 5 percent dividend stock has likely stopped growing which means it has no use for the profits it makes. It hence is returning those profits as dividends to shareholders. The stock then starts to act like a bond without the safety of a bond.

And if a stock was yielding 2 percent dividend and in a few short months, the yield jumps to 10 percent, there is an even bigger problem. How does a stock go from yielding 2 percent to 10 percent in a short amount of time? When the stock price drops by 80 percent. When does a stock price drop by 80 percent? When the market thinks that the business behind that stock is going to go out of business. What is likely to happen to that dividend? It will be cut because the business is now in survival mode. It would want to retain all the cash it has.

What you want are natural dividends that are an outcome of the capital allocation decisions businesses make. In other words, you want the businesses you own to do everything they can to grow the business, explore all growth opportunities and only when there is none growth left should they return cash to the shareholders.

We then delve into other more exotic strategies where investors go hunting for yield but just as before, promised yield is not realized return. A popular one amongst them is writing covered calls against a stock you already own.

So say you own 100 shares of a stock that trades at $28 a share and you sell a 90-day call option against those shares with a strike price of $30. And say the buyer of that option pays you 50 cents a share as premium to exercise that right.

So you now have $2,800 of the stock plus $50 in cash (50 cents per share in premium x 100 shares). If in 90 days, the stock price stays below $30, the call option expires worthless and you get to pocket the $50 premium. Plus you still own the shares.

But if the stock price hits $32 in 90 days, the stock gets called away at the agreed upon price of $30. You still get to keep the premium and the $2 per share in profits between the original price of $28 and the strike price of $30 but you lose the $2 more per share in upside at the new stock price of $32.

I know it sounds confusing but the best part is, you don’t need to know any of this. In fact, I wouldn’t even try. Because there are two things you must remember when trying anything exotic with your money…

- Most are zero-sum games and that is before taxes and transaction costs. For you to win, someone at the other end must lose. And that someone is no dummy. It is more likely a Citadel or a Goldman Sachs with math PhDs, equipped with an arsenal of data and computers. You are their catch.

- You are guaranteed to lose in the long run against owning a sensible portfolio of stocks and bonds that matches your station in life because these strategies promise something that cannot happen – capital preservation and growth. These two phrases in the same sentence separated by an “and” in the middle do not exist.

I came across this image below, don’t know who the creator is but it perfectly describes what is wrong with all these strategies.

NAV stands for net asset value. It is the per share price of an ETF on a given day.

The only place where the promised yield equals the realized return is when buying treasury bonds. They carry no credit risk. The interest rate you buy the bond at is the yield you get.

Treasury bonds also make ideal benchmarks to compare all investments against. If a 10-year treasury bond is yielding 5 percent and you find an investment that yields 7, you know there is a risk. And the risk rises as the yields rise. Nothing wrong with that, just that you should know where that extra yield is coming from.

And if you see the word guarantee in any investment being pitched that are not treasury bonds, you’ll have a problem. Because when anything sounds too good to be true, it usually is.

Thank you for your time.

Cover image credit – Owen Outdoors, Pexels